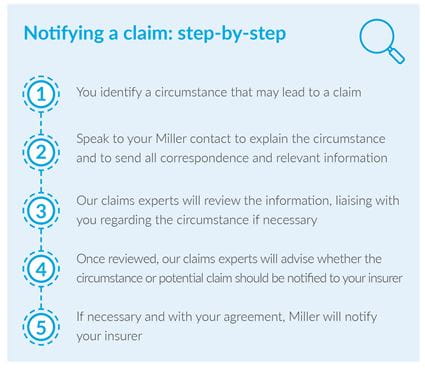

If in doubt: ‘Always contact Miller’ is the golden rule when notifying a professional indemnity insurance (PII) claim.

We are here to advise you on the best way to handle any potential notifications. The wording of your policy will determine how a notification should be handled and it is important to note that not all events are notifiable.

The conditions of most policies require you to provide prompt notice of circumstances which may result in a claim. Failing to do so could result in insurers repudiating your claim due to late notification. Again, if you are unsure, please contact us for advice.

Who, what and when to notify

There is no definitive list of potential notifiable circumstances, however the

common ones we experience are:

- Any ‘circumstances’ that may lead to a claim

- Any complaints being dealt with through a formal grievance procedure

- A formal complaint or letter before action - even if the threat of following through is ambiguous or verbal

If you experience any of the above events, notify your Miller contact as soon as you become aware, regardless of your views on liability or the sum involved.

We have a wealth of experience in handling such matters, so if you have any doubts as to whether something should be notified or not, please contact us immediately.

What you must NOT do

When you become aware of a claim or circumstance, there are certain rules you must follow to avoid a potential breach of your policy terms and conditions:

- DO NOT admit liability

- DO NOT settle or offer to settle the claim

- DO NOT disclose your insurer’s involvement or details of your PII

- DO NOT take any action which could prejudice your insurer’s position or their ability to investigate the claim or circumstance

- DO NOT enter into correspondence with the claimant without your insurer’s permission – insurers must approve all correspondence prior to it being released

Late notification

If an insurer deems a claim or circumstance has been notified late, it may be because of three potential issues:

- The notification should have been made earlier

- You have changed insurers and the current insurer deems that previous insurer should be dealing with the claim

- The policy has expired and therefore the notification is out of time